Regulation Supplement

Aug 25, 2016

To ensure smooth, fair and honest operation within the market

Regulation drives market efficiency

By Faridah Kulabako

Imagine what would happen to Kampala city without a regulator for just a week. Mountains of garbage would be littered everywhere, taxis would park anywhere, including in the middle of roads to load and offload passengers and hawkers would jam all streets.

Markets free of regulations are sometimes chaotic and can be exploitative. Such markets also tend to be characterised with uncompetitive practices and can also lead to monopolistic tendencies. Thus, regulation is important in any market to ensure that businesses operate and compete in a fair manner.

Additionally, regulation is used to achieve social, political, environmental and economic outcomes that would otherwise not be achieved within the market. Thus, the goal of regulation is to ensure a smooth, fair and honest operation within the market.

However, having regulations without implementing agencies is not enough; there is need to have authorities to enforce the rules and ensure that regulation works effectively and is in the public interest.

Uganda has a number of regulatory authorities that enforce standards in their respective sectors. The financial sector is regulated by the Bank of Uganda, which oversees commercial banks, credit institutions, and micro-finance deposit taking institutions.

The Insurance Regulatory Authority regulates insurance companies. The Uganda National Bureau of Standards which is charged with enforcing standards in trade and industry to encourage fair competition and protect consumers.

The Capital Markets Authority is responsible for promoting, developing and regulating the capital markets industry, with an overall objective of protecting investors and ensuring market effi ciency.

The Uganda Retirement Benefits Regulatory Authority that was established to regulate the establishment, management and operations of retirement benefi t schemes in Uganda both in the private and public sectors, is also charged with promoting the development of the retirement benefi ts sector.

The National Environment Management Authority is charged with the responsibility of co-ordinating, monitoring, regulating and supervising environmental management in the country.

The Uganda Coffee Development Authority is mandated to promote and oversee the coffee industry by supporting research, promoting production, controlling coffee quality, and improving the marketing of coffee in order to optimise foreign exchange earnings for the country and payments to the farmers.

The Dairy Development Authority is mandated to develop and regulate the dairy industry in a sustainable manner. The Uganda Revenue Authority is charged with the assessment and collection of taxes, administering and enforcement of the laws relating to such taxes.

The Kampala Capital City Authority governs the capital city and administers it on behalf of the central government. The Electricity Regulatory Authority is charged with establishing a tariff structure and to investigate tariff charges, approve rates of charges and terms and conditions of electricity services provided by transmission and distribution companies and to develop and enforce performance standards for the generation, transmission and distribution of electricity, among others.

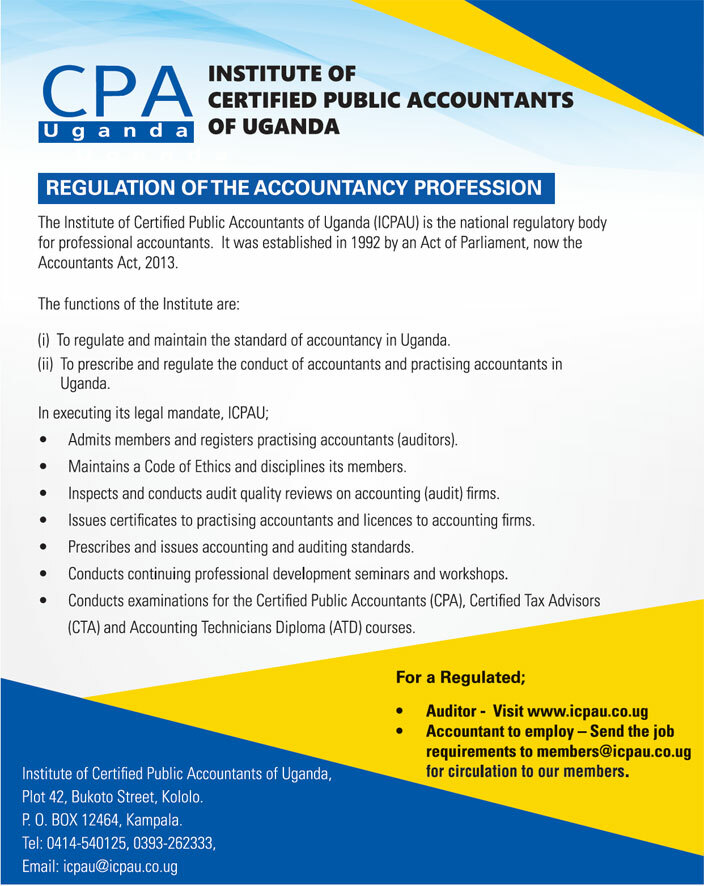

There are other agencies that ensure good practice. For example, the Institute of Certifi ed Public Accountants - Uganda regulates and maintains the standard of accountancy in Uganda by prescribing and regulating the conduct of accountants. The other such bodies include the Uganda Law Society and the Uganda Health Monitoring Unit.

PROTECTING CONSUMERS OUR PRIORITY - INSURANCE REGULATOR

Faridah Kulabako

Having tried to seek compensation from an insurance company over a period of 12 months for an accident he was involved in, Benon Oluka, a journalist, raised his complaint in the media after his efforts hit a snag.

Though he had not engaged the Insurance Regulatory Authority's (IRA) complaints bureau directly, he was called and requested to meet their legal team and the insurer's representative to resolve the matter amicably.

After listening to both sides, the bureau advised the insurance company to pay him sh5m in compensation for the bodily injuries sustained in the April 2015 accident on the Mubende-Kibaale road, because the vehicle he was travelling in was comprehensively insured.

Compalints bureau

The complaints bureau is one of the avenues that were set up by the regulator to provide a medium for amicable settlement of complaints between the insurer and the insured. IRA, through the bureau, received 160 complaints from insurance consumers last year, with the biggest number (45) related to delayed claims payment followed by unsatisfactory medical services at 17.

Figures from IRA indicate that by December last year, 66 out of the 160 registered complaints had been settled. On the other hand, 28 had been closed for various reasons such as failure by complainants to provide enough information, 52 were still pending, while the rest were subjudice.

The reluctance by some insurers to pay clients' claims had eroded public confidence and tainted the insurance sector's image. This partly explains why the insurance penetration rates in Uganda are the lowest in the East African region, estimated at 0.85%, compared to Kenya's 3.7%, Rwanda's 2% and Tanzania's 1%.

It should also be noted that the industry has also undergone numerous regulatory reforms over the last five years so as to create a conducive environment to build a financially strong industry that meets both the insurers and the insured's needs.

Although many road accidents occur in Uganda, very few people claim third party compensation from insurance firms

Although many road accidents occur in Uganda, very few people claim third party compensation from insurance firms

For instance, following the amendment of the Insurance Act that saw the Uganda Insurance Commission rebrand to the Insurance Regulatory Authority (IRA) in 2011, tight deadlines for claim settlement were introduced to help restore confidence in the sector.

The reforms, for instance, required insurance companies to pay claims of up to sh10m within 10 working days after receipt of discharge voucher. Claims of between sh10m and sh50m must be settled within 15 working days while those above sh50m should be paid within 20 working days after receipt of discharge voucher or upon receipt of cash call payment from reinsurers, whichever occurs first.

It should be noted that the sector's image had suffered due to perceptions that insurance firms do not pay claims. This has eroded consumer confidence in the sector, constraining the uptake of insurance services.

The Insurance Institute of Uganda chief executive officer, Elvis Khisa, however, says although the industry's image had been tarnished due to failure to pay claims, it is slowly improving following tough actions taken by IRA to punish non-compliance.

IRA has in the past suspended or revoked operating licences of non-compliant insurance firms and those that fail to pay genuine claims. For instance, it withdrew the Africa Premier Health (APH) operating licence last year over failure to pay claims and poor services to its clients.

The Rio Insurance licence was also suspended last year over conduct-related issues. The IRA chief executive officer, Ibrahim Kaddunabbi Lubega, says the authority's mandate is to protect policyholders' interests. By cracking the whip, IRA seeks to send a strong signal to all potential non-compliant players.

The other regulatory reform undertaken to enable players pay claims promptly was increasing the minimum capital requirements, to which all players complied by September 2014 set deadline.

The directive, which sought to build a financially strong insurance industry, required insurance companies underwriting the life insurance business to increase their minimum capital to sh3b and sh4b for non-life underwriters, up from sh1b, each.

Reinsurers, on the other hand, were required to have minimum capital of sh10b from sh2.5b, while brokerage firms increased to sh75m, up from sh50m. IRA noted that prior to increasing the minimum capital requirements; some insurance companies had very low retention ratios, requiring higher capital to improve retention ratios.

The changes also saw the six insurance companies that were offering life and nonlife insurance as a composite business; separate them in October 2014. The move to separate the businesses further sought to strengthen the industry and improve its performance.

Also, the health membership organisations (HMOs) - the medical segment of insurance - got guidelines in October last year as the regulator moved to strengthen their fi nancial positions to sustainably handle big health insurance policies. The new guidelines require HMOs to have a minimum capital of sh20m this year, sh250m by the end of this year, and sh500m by 2017.

Amending the act

Promised action: Kaddunabbi

Promised action: KaddunabbiIRA is also currently amending the Insurance Act in order to align it with the global insurance core principles (ICPs) and eliminate the issuance of annual licences to industry players in favour of continuous ones.

According to Kaddunabbi, enforcing ICPs will enable insurers attract more business by creating confi dence in the industry, which will in turn boost insurance penetration rates. The Lion Assurance managing director, Newton Jazire, notes that the regulatory reforms undertaken by IRA in the last fi ve years have created a good regulatory environment which has enabled innovation and quicker settlement of claims.

A similar view is shared by Liberty Life Assurance managing director Joseph Almeida, who says the conducive regulatory environment has facilitated sector growth over the last fi ve years. Insurance premiums have for instance grown from sh239.99b in 2010 to sh611.1b in 2015.

Gaps

Insurers, however, urge the regulator to partner with them to enhance consumer confi dence and thus boost uptake of insurance services. Their values are shared by Oluka, who says most people, especially bodaboda riders who are the biggest victims of road accidents, do not claim compensation because they do not know their entitlement.

"IRA needs to enhance public awareness, so that people know that they are supposed to seek compensation in case of accidents. They should also tell them where to seek redress in case insurance companies refuse to pay," Oluka says.

Despite being the most widely bought insurance policy, because it is compulsory, analysts say only about 7% of motorists claim compensation, partly because of the low compensation limits.

Petitioned regulator: Oluka

Petitioned regulator: OlukaAccording to Nicholas Smith, a consultant at the World Bank, insurance firms in Uganda pay only 2% in compensation annually, leaving 98% as profit to insurance firms. Uganda has one of the highest road accident rates in Africa estimated at 17,000, annually.

IRA is in the process of overhauling the Motor Third Party (third party risks) Act, 1989, so as to increase the compensation limits from the current sh1m and make it more attractive to policyholders.

It also seeks to increase the compensation limits for victims and broaden the scope of cover to cater for all injuries, deaths and damage to property caused by motorists. Also, the scope of the cover is limited to only bodily injury and not property damage and drivers among others, but the proposal is to broaden it to benefit all the affected persons.

However, Jazire cautions that IRA against opening up of the Motor Third Party liabilities as it might stifl e sector growth since Uganda is still a young market. He also says the regulator should go slow on adopting risk-based supervision as it may hinder sector growth.

IRA is in the process of shifting the supervision model from compliancebased — where insurance companies simply meet the set benchmarks, irrespective of risk levels — to risk-based supervision — where insurers take on insurance risks based on their financial capacities. The model will see some fi rms that insure bigger risks have bigger capital requirements than those with smaller risks.

"Risk-based supervision should not be rushed; it should be taken step by step instead of forcing it on players. Also, there is a proposal to open the Motor Third Party compensation limits, but that cannot work in a market like Uganda, it is for developed economies," Jazire notes.

|

Lion Assurance managing director Newton Jazire urges IRA to put in place tougher penalties such as premium undercutting to indiscipline. "A penalty of sh1m or sh2m is nothing to an insurance company; the regulator needs to get tough and give a hefty fine," Jazire says. Responding to players' concerns, IRA communications officer Mariam Nalunkuuma says tougher penalties for indiscipline are provided for in the Insurance Amendment Act, which is yet to be approved by Parliament. She adds that the shift to risk-based supervision seeks to align Uganda's insurance sector with its East African counterparts, so as to enable harmonisation of region insurance services as per the EAC common market protocol. About opening up the motor third party limits, Nalunkuuma notes that the proposal to increase compensation limits and scope of coverage seeks to ensure that the victims get fair compensation. "Our major role is to protect policyholders' interests; the current limits are too low and people see no value in going through a lengthy procedure to claim sh1m which can barely fully cover one's medical bill in case of a major injury. "We want the limits increased so that we entice policyholders to claim compensation because it is their right," she explains. |

Standards body facing hurdles

By Prossy Nandudu

Even with the presence of the Uganda National Bureau of Standards (UNBS), complaints abound of all kinds of breaches to standards ‑ from substandard consumer goods to construction materials.

The head of UNBS, Dr Ben Manyindo, agrees there is a problem but blames it on a number of issues, mostly funding and the structure of the standards body itself. He also suggests radical changes that would see UNBS staff work four times as much to stem the growing public concerns about standards.

According to Manyindo, UNBS operates on a budget of sh20b annually for salaries, infrastructure development, financing operations, surveillance and training of small to medium enterprises (SMEs).

"That money is not sufficient. "If you divide sh20b among 36 million Ugandans, each would get about sh600 a year, yet to be safe, the maximum should be sh3000 per Ugandan per year," said Manyindo.

However, to get out of this situation, Manyindo suggests that transforming the bureau into a trade support organisation would solve a lot of its problems. Currently, it is a public service institution, whose funds are just a small portion of the budget of its mother Ministry of Trade, Industry and Cooperatives.

As a trade support organisation, it would move from working eight hours a day, five days a week like all civil servants institutions to working 24 hours a day, seven days a week. "Unless we are allowed to shift from a public service oriented institution, so that we can increase staff numbers to support the institution, we shall remain inefficient since we only have one person out of the four that is required," Manyindo said.

PRIORITIES

Manyindo said UNBS identifies key priority sectors to quickly respond to first and to others later when resources allow. The priority areas include foods and beverages, because these affect lives directly and electricals, which can be quite dangerous because of house fires. These are followed by cosmetics for which they have acquired new testing tools and lastly construction materials.

CULPRITS

- In it research, UNBS discovered that most of the fake or substandard products on the market are imported. According to Manyingo, even with the institution of the pre-export verification of conformity to standards measure, some unscrupulous people smuggle in undesirable products

- The other culprits are local manufactures operating in their backyards without supervision and monitoring. Manyindo said when these people are caught; they usually plead lack of funds to operate according to requirements. lThe third culprit is the traders whose products expire on shop shelves but they recycle them, repack them and return to the market.

- The fourth that could be the most dangerous are those adulterating products like cement, which they mix with clay and clean water mixed with dirty water, among others, to increase quantities. So, according to Manyindo, the work is enormous, yet the facilities and the manpower are limited. He points out that the labs, for example, are small and not adequately equipped yet the volumes of products to test keeps growing. On staffing, he says, out of 160 entry points, UNBS' presence is only on 17, which is about 10%. So, whether the changes that Manyindo suggests would deliver can only be ascertained if they are instituted, but currently the UNBS has to be creative and do with what it has.

Securities exchange: Uganda's idle gold mines

By Samuel Sanya

A number of businesses are pleading with the Government for a bailout saying they are faced with a real risk of collapse which could impact the economy and jobs. They attribute their woes to a tough business environment and punitive interest rates.

But as Uganda battles with the rising tide of bad and doubtful bank loans, it should be noted that there is cheaper, longer-term capital on the equity markets. The ultimate role of Uganda's capital market is to provide alternate means of raising long-term fi nance, which in turn boosts enterprise, job creation, and household incomes to provide impetus for the Vision 2040 master plan of a middleincome Uganda by 2020.

Capital markets deal with the trading of financial products such as company shares, bonds issued by governments or private companies, units in Collective Investment Schemes, debentures, commercial paper and notes.

These financial products can also be referred to as securities and are generally traded on a stock (securities) exchange. The capital markets are regulated by the Capital Markets Authority (CMA).

Through it , the Government is encouraging the development of the capital markets industry as a way of generating longterm capital to promote sustainable growth, mobilise savings and broaden the availability of funds for investment purposes. The CMA was established in 1996 as a semi-autonomous body responsible for promoting, developing and regulating the capital markets industry in Uganda, with the overall objectives of investor protection and market efficiency.

It also advises government on all policies concerning the development and operation of the capital markets industry in Uganda, and formulating guidelines for the proper conduct of the securities business in Uganda.

In addition, it formulates guidelines and rules for companies wishing to list and sell shares to the public, and the protection of investor interests. In its role as a regulator, the CMA oversees the activities of the Uganda Securities Exchange (USE), the ALTX securities exchange, licensed intermediaries such as brokers/dealers and investment advisors.

The capital markets help mobilise domestic savings, and in so doing, the market facilitates the reallocation of fi nancial resources from dormant to more productive activities; from investors with excess capital to companies with profi table ventures.

In the 1990s, the capital markets provided an avenue for the divestiture of State- Owned Enterprises (SOEs) and some of its shares jointly held in other entities like Bank of Baroda, National Insurance Corporation (NIC), dfcu and the New Vision.

Thus, members of the public participated and own part of these bodies. The capital raised was, therefore, used by those entities to expand production, invest in more effi cient productive processes and improve competitiveness.

Vision group's Robert Kabushenga speaking as the Uganda Securities Exchange manager legal and surveillance department, Judy Obitre Gama, looks on during a training of Security Exchange brokers on May 25, 2008

Vision group's Robert Kabushenga speaking as the Uganda Securities Exchange manager legal and surveillance department, Judy Obitre Gama, looks on during a training of Security Exchange brokers on May 25, 2008

This increased investment should feed into employment expansion, income generation, and with a larger percentage of the population earning incomes; savings and consumption would increase, followed by increased investment, increased production, enhanced economic growth and wealth creation.

It encourages full disclosure by the companies, better accounting and management practices, greater transparency in the business sector and lower incidences of corruption.

ACHIEVEMENTS

In 2012, the CMA shifted from compliance-based to a riskbased supervision approach which created more efficiency. Uganda now has two licensed securities exchanges, 16 listed companies, half of them local, two securities central depositories and 25 brokers/investment advisors/ collective schemes.

The second securities exchange, the ALTX, of 2016 operates on world class software and is tipped to also act as an electronic commodities exchange to expedite trade in grain and derivatives. Derivatives are fi nancial instruments whose price is based on a product, Warehouse receipts are the commonest derivative in Uganda.

The value of the receipts, which can be sold, depends on the prevailing market price of maize, coffee, or beans in the warehouse. During ALTX' official launch in Kampala, CMA chief, Keith Kalyegira advised that the trade ministry could use it as the commodities exchange instead of creating a new one.

Its chairman, Edward Mugwanya, said ALTX Uganda aims to encourage a saving culture that would push Uganda to the middle income status. He says it is eyeing 10 million accounts in the next five years. The chief executive of USE, Joseph Kitamirike, agreed noting that it will be aided by Uganda's youthful population.

According to data from the Uganda Bureau of Statics (UBOS), over 70% of Uganda's 36 million people are under 30 years and 52% is below 15 years. The amendments to the CMA law this year introduced new categories for approvals and licences which ideally look to improve efficiency and attracting more players, according to Nsamba.

Chief Justice Bart Katureebe, who was then board chair for New Vision, rings the bell at the listing of the New Vision on the securities exchange on December 16 2004. Looking on are Onegi Obel (left), William Pike and Robert Rutaagi.

Chief Justice Bart Katureebe, who was then board chair for New Vision, rings the bell at the listing of the New Vision on the securities exchange on December 16 2004. Looking on are Onegi Obel (left), William Pike and Robert Rutaagi.

Besides the amendments, also created a Capital Markets Tribunal to handle and resolve related disputes here. There will also be whistleblower protection in case any breaches of securities laws are reported.

It also creates a Fidelity Fund to insulate the securities exchange from liabilities arising from wrongs committed by employees of the securities exchange. The CMA will administer the fund which will operate a Bank of Uganda licensed account.

CHALLENGES

Twenty years in existence, capital markets are still struggling to enlist a critical mass of Ugandans. The shallow and under developed nature of the financial sector is often cited as a major stumbling block.

According to Andrew Mwima, the USE trading manager, there are only about 28,000 accounts with the USE securities depository, 50% of them held by Kenyans. Ugandans hold less than 10,000 and the rest belong to foreigners.

But finance minister Matia Kasaija says things can improve with sensitisation of Ugandans on wealth creation and raising business capital through capital markets. He noted that in the region, Kenya leads the pack with 2.5 million securities accounts followed by Tanzania with 250,000 and Rwanda with 200,000.

"We Ugandans are very poor savers and spendthrifts. Someone can spend sh100,000 in five minutes without saving some for the future or purchasing something of value with it," Kasaija said. It is evident that the CMA still has a big task of attracting more Ugandans, which would in turn feed Uganda's development goals.